North American markets are entering the second quarter of 2026 with heightened volatility as sector rotations increasingly shape equity performance, according to analysts. Despite the S&P 500 trading within a 7% range, significant shifts are occurring beneath the surface, reflecting investor caution amid geopolitical and macroeconomic uncertainty.

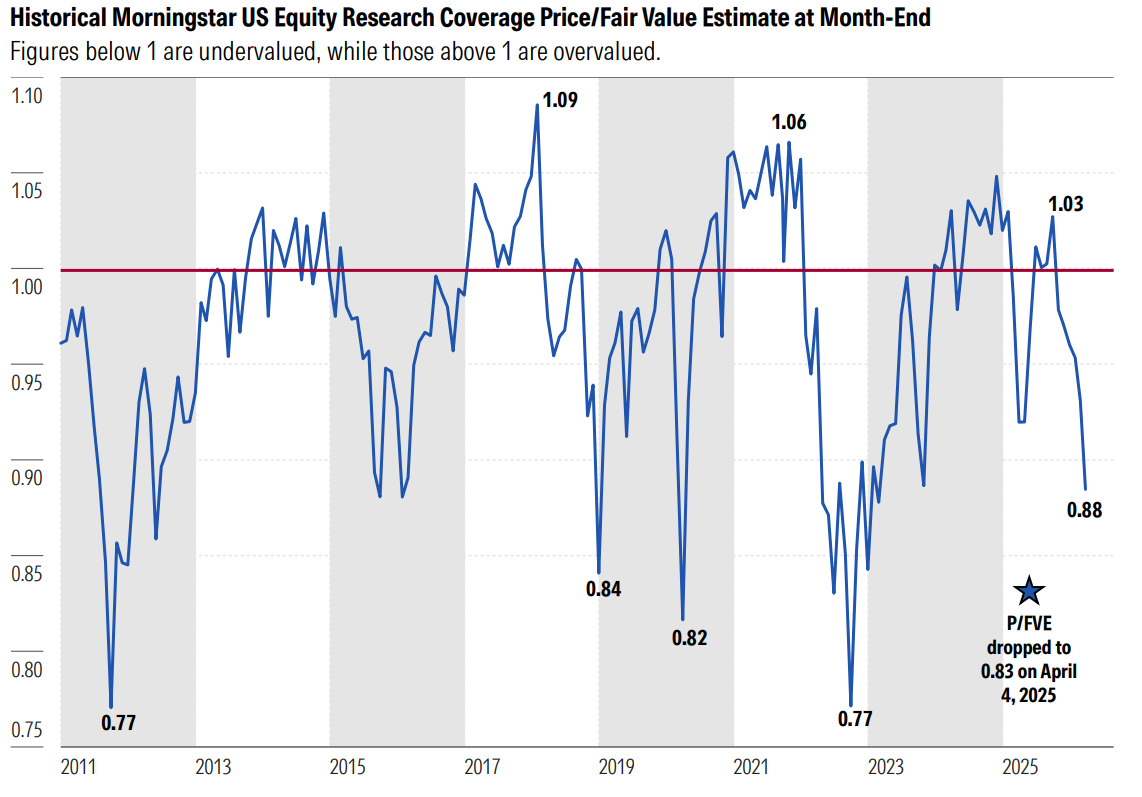

Dave Sekera, Chief US Market Strategist from Morningstar, noted that valuations remain attractive with equities trading at a 12% discount to internal estimates. Market rallies, however, have largely depended on developments in the ongoing conflict with Iran, with investors awaiting a public signal that Tehran is open to negotiations.

The AI investment boom, which has fueled market optimism for the past two years, is now facing a period of reassessment. Analysts believe that the next leg of growth for technology stocks will require clearer evidence that capital spending on AI is translating into revenue expansion and improved operating margins.

Meanwhile, elevated oil prices and persistent inflation pressures are challenging corporate management teams as they prepare to issue first-quarter guidance. Many are expected to adopt a conservative stance to account for rising uncertainty and potential cost pressures.

With growth slowing and interest rates edging higher, the Federal Reserve remains in a difficult position, constrained from cutting rates without risking inflation or raising them without jeopardizing economic momentum. The upcoming earnings season, starting the week of April 13, is anticipated to provide deeper insights into how companies are navigating these shifting market dynamics.

{kind=link}